There’s one thing in common for those looking to open a TD e-Series account by mail or by person: you’ll need to answer a couple questions in the Investor Profile Questionnaire. The purpose of the questionnaire is to assess the comfort level of the investor and to assign a general target asset allocation.

If you opt to mail in the application to open the e-Series account, you’ll need to fill out the application form. The form includes instructions on how to determine your recommended allocation and you can modify the answers as many times as you like to get the asset allocation that you want.

If you’re opening an e-Series account in person at a branch, a bank representative will take you through the questions. If you don’t get your desired asset allocation, you can ask the representative to change the answers until you get your desired allocation if they allow it.

Filling out the questionnaire can be a little tedious and was frustrating the first time I wanted to open an account. Let’s take the guess work out of the equation and answer the questions to get the asset allocation that you want.

A Primer on Asset Allocation

When investing, portfolios are generally made of two components: Equity (i.e. stocks) and Fixed Income (i.e. bonds). The asset allocation is simply distribution of equity and income. Picture a pie chart where 60% of the money in a portfolio is used in equity with the remaining 40% in fixed income. The decision on how to divide money between the two is a personal one and depends primarily on investment goals, age, and risk tolerance among other factors.

TD e-Series: Filling out the Investor Profile Questionnaire

The investor profile will determine the recommended asset allocation to which the account will adhere. For example, if your investor profile results in an asset allocation of 60% Equity and 40% Fixed Income, the account may not let you make purchases that exceed this ratio. Equity can not be held in excess of 60% of the portfolio value. That being said, equity can be held amounts less than 60% without any issue. Other asset allocations that can be accommodated are 80% Equity / 20% Fixed income and 100% equity.

Whether in person or by mail, the first series of questions (Section A in the application form) are intended to provide the bank a snapshot of your investment knowledge and current financial situation. These answers do not go towards the calculation that determines the investor profile.

The subsequent questions are broken up into three sections: B. Portfolio Objectives, C. Time Horizon and D. Risk Tolerance. Answers given in each of the sections correspond to a series of points. The sum of the points in each section determines the investor’s profile and target asset allocation.

Keep track of the points for later use when filling out the form to mail in. You do not need to keep track of the points when apply in a branch the tally is done automatically.

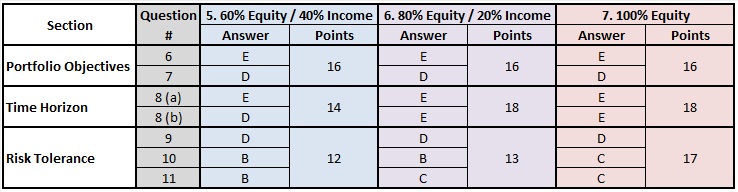

Answers for a 60% Equity/40% Fixed Income Allocation

For a 60% Equity / 40% Fixed Income result, provide the following answers to these questions:

Section B. Portfolio Objectives

- Which of the following best describes your objective for this account? E

- How important is it for you to keep a portion of your account in relatively safe investments with minimal fluctuations? D

Providing these answers will result in 16 points.

Section C. Time Horizon

8a. How many years do you expect to be saving before beginning to withdraw from this account? E

8b. How many years do you need the funds in this account to last once you begin withdrawing? D

Providing these answers will result in 14 points.

Section D. Risk Tolerance

- Which of the following best describes the type of investments you currently own, or have owned in the past? D

- The charts below show hypothetical annual returns for three different investments over an 80 year period. Keeping in mind how the returns fluctuate, which investment would you be most comfortable holding? B

- Investments with higher returns typically involve greater risk. The following chart shows four hypothetical investments of $10,000, each with a different potential best and worst outcome at the end of one year. Which investment would you be most comfortable with? B

Providing these answers will result in 12 points.

How TD Determines the Investor Profile

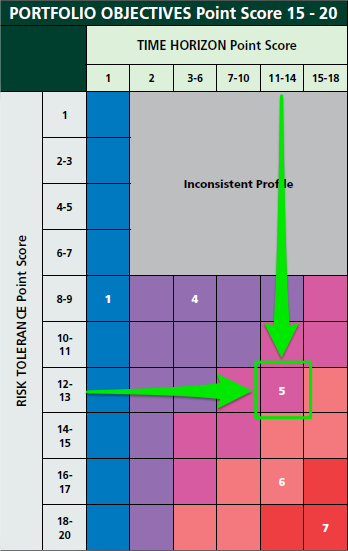

The points from each of the above sections are used to determine the investor profile. Again, the points are summed automatically when applying for an account in person, but need to be recorded when applying by mail. The 16 points scored in Section B. Portfolio Objectives results in the use of the below table. Plotting a vertical line from the points scored in C. Time Horizon (14) to a horizontal line drawn from D. Risk Tolerance (12) point to an investor profile of 5.

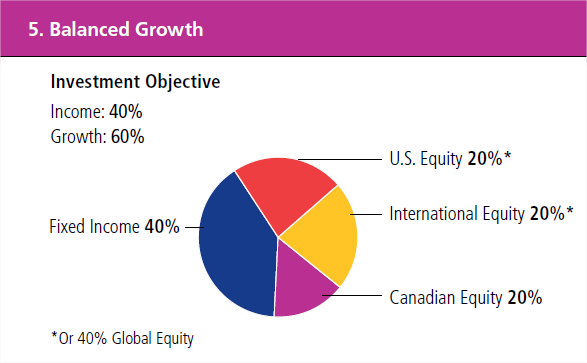

Investor profile 5 recommends a Balanced Growth portfolio with the allocation we set out to achieve: 60% equity, 40% Fixed Income.

TD Investor Questionnaire Cheat Sheet

It isn’t rocket science to go back and determine the answers that correspond to asset allocations with higher percentages in equity. To make things simple, here’s a little cheat sheet to get the asset allocation that you want.

The Last Word

Now that you know how to ace the investor profile questionnaire and are well on your way to opening TD e-Series account, you’re ready to buy the TD e-Series index funds!

Disclaimer: The content within this post is based on my experience and is provided for information purposes. It is not intended as investment advice. For investment advice, please consult a professional.

I hate these investor profiles, Tangerine does the same thing.

That being said I suppose it does help those who are clueless. I’m using TD Investments so no profile required =D. In the new year I may switch to ETF’s. I’m rapidly approaching the $100K mark in my RRSP but have been lazy to switch so far.

I’m considering a switch to ETF’s soon as well. There’ll be all new paper work come that time!

This is a very helpful guide. Thanks Daniel!

Thanks!