It’s midway through spring and the sun is finally out, seeping into every corner of our little condo. While the sunlight is lovely and much welcomed, it has revealed the some ugly truths: our home is looking rather grim. There is so much dust collecting under furniture, our cream-coloured couch is more day-old cream than its former freshly poured white, and there are little handprints on practically every mirror and windowpane. It’s time for spring cleaning.

It’s not just our fixtures that need some sprucing up; our financial budget is in need of tidying as well. It’s time for a budget re-balance.

Budget Review

We took a look at our trends over the past six months and found the following:

- Monthly exceedances in Food costs

- Monthly under runs in Transportation costs

- Savings rate increased from previous year and in line with 2014 goals

- Emily borrows months worth of personal allowance from Daniel, blows it all on clothes, and doesn’t spend until debt is repaid. Rinse and repeat.

- Daniel doesn’t spend money. Instead, his personal allowance continues to roll over. Apparently he’s saving up for some big electronic gadget.

Budget Re-balance

Based on the trends, we’ve decided to make some changes. We’re going to increase our Food budget. With a growing kid whose appetite rivals mine on some days, we are okay with spending more on groceries. The amount allocated to eating out will remain the same even though we tend to exceed it; we need to work harder at keeping our eating out expenses within budget.

Our transportation budget will be decreased. From working either at home 1-2 times a week, at client offices, or travelling for business, we’ve decreased our gas and public transportation expenses. Not by much and it does vary week to week, but on average, the decrease in transportation expenses equal the amount we’ve been exceeding our grocery budget.

We both received raises in the last six months. Despite the increase in income, we’re trying to avoid lifestyle inflation and keeping the expenses the same and thereby increasing our savings rate by a couple of percentage points.

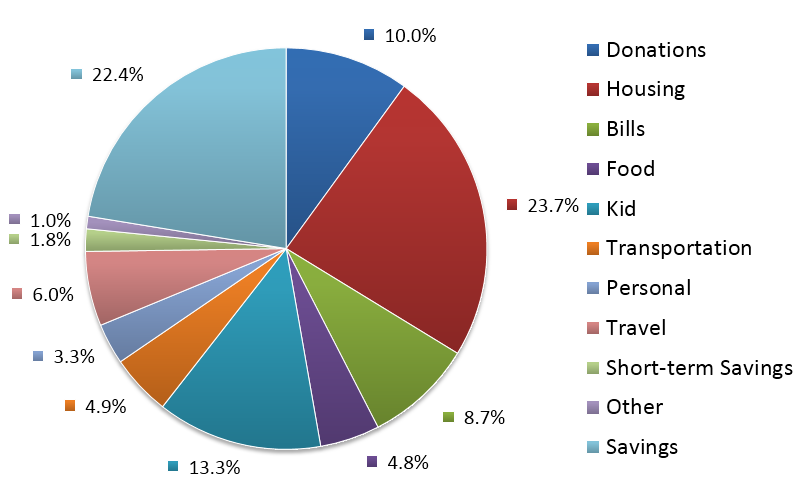

The New Budget

Here is our new budget allocation (percentages are based on net income):

[table]

[table]

Item, Percentage, Description/Comment

Home, 24%, “Biweekly mortgage, additional mortgage payments, home insurance, property tax”

Savings, 22%, “TSFA, RESP, RESP contributions”

Kid, 13%, “Daycare and other”

Donations, 10%, “Tithe/offering to church, charitable organizations”

Bills, 9%, “Cell phones, internet, maintenance fees”

Travel, 6%, “Annual travel fund contribution”

Transportation, 5%, “Car maintenance, car insurance, gas, public transportation costs”

Food, 5%, Groceries and eating out

Personal, 3%, “Entertainment, personal allowance”

Short-term savings, 2%, “Christmas and wedding presents, other”

Other, 1%, Buffer[/table]

(Compare our current budget with our previous budget)

Importance of Analyzing a Budget

Creating a budget and regularly tracking expenses is just the first step in improving upon your financial health. The next steps of analyzing and re-balancing budgets are just as important.

Analyzing the budget gives us a clearer picture of our habits and can allow us to make better financial decisions based on the past behaviours. We’ve identified some patterns in our spending habits and are exceeding the budget in some areas.

We know what areas need work and have mutually decided to make appropriate adjustments through rebalancing. Budgeting is an ongoing and reiterative process; it is not meant to be stagnant, but dynamic to reflect current financial status, habits, and goals.

Last Words

We created and started following a budget when we first married. We had a school loan to pay off and Daniel was laid off of work, living off a single income and Employment Insurance. We lived minimally. We didn’t eat out and we didn’t spend anything on ourselves. The sacrifices were worth enduring as we wiped out the debt in about twelve months.

Since then, our priorities have shifted. We no longer have a student loan but we still have a mortgage. We have a lot more to work with than we did back then, but we also have retirement to think about. It is no longer just Daniel and I, but we also have an additional mouth to feed and send to daycare. Our financial situation has change as well as our focus. We continue to track our spending, analyze it and rebalance to achieve our financial goals.

When was the last time you re-jigged your budget?

Rejigged in February just before Baby Bun arrived although my rejigging is more: Spend as little as you can! Look at your dwindling emergency fund.. GAAAAH!!!!! FIND A CONTRACT the minute he turns 3 months old!!! Work work work then get pregnant again and have Child #2!!!! MUST WORK BEFORE!

Yep. That kind of rejigging.

I backwards budget – I don’t have targets to stay under, I just pay $500 for rent and food to our shared account, and $500+ to my mortgage (which is also my savings, as it sits in an offset account which is drawn on monthly for the repayment). Otherwise, I allow myself about ~$120 walking around money – eating out, snacks, coffees etc. Clothing and gifts are ad hoc, sometimes out of the $120, sometimes out of ‘what’s left’ in the bank account for the week (or on credit card, which is paid off weekly). i also ‘save’ targetted for annual health insurance premium, auto savings for charity (some straight to church, some earmarked for ‘big’ contributions), auto savings for bills on the property I own. All my retirement savings are done pre-pay (ie automated through payroll), but are above and beyond the average!

Anyhow… I think I might look at the $s I spend as a percentage of my take home, and look at if I can set a higher benchmark for savings. I’m not in debt other than the mortgage, but every cent I put in the offset is minimising my interest, and it’s still cash I can draw for savings, a new TV or the like. I like pie graphs too… so perhaps that’s a drawcard to.

Oh and I know, one day, there’ll hopefully be a wedding, and babies, and the cash is doing well there.

I just re-jigged the budget last week when I realized my take-home was going to be a bit lower after deductions. I’m still saving around 12-15%, and putting about 35% to debt, so it isn’t horrible. It’s nice to know there is enough wiggle room in there to absorb those sort of changes.

I’m loving your blog Emily! I’m finding a lot of similarities, in that Eric and I also had to live off one income for various reasons (education, work injury, etc). Times were tough! We’re doing much better now but still saving a ton so we can save up for a house.

Yes, we lived on one(-ish) income when we first married, and it was hard! (note, I say -ish because we did receive unemployment insurance and Daniel found a temp job six months unemployed to ease finances, but all the while still looking for something in his industry). We lived in a furniture-less home and ate pasta and tomato sauce for dinner almost every day. Haha. I love how you’re embracing your debt-free life and enjoying it with a bit of lifestyle inflation. I’m all for spending as long as there as finances are in order and a plan is in place, which seems like the case for you.