Management Expense Ratio Explained

The management expense ratio (MER) is the cost of managing and operating a mutual fund. The MER, by definition, is the ratio between the sum of the management fee and operating expenses divided by the total value of assets held within the fund (or portfolio value); it is expressed as a percentage of the portfolio value.

Note, MER does not factor the cost of trading securities into account; that is a separate fee charged to investors known as the trading expense ratio (TER) which will not be discussed in this post.

How is MER Calculated?

Let’s take a look at the TD Canadian Equity Fund (TDB161). According to the fund facts, the portfolio value as of June 30, 2013 was $2,467,591,691 and the MER was 2.18%. The date (June 30, 2013) indicates the last time the MER was calculated for the fund; the MER is considered a historical value of expenses incurred and is used as a best guess of expenses moving forward until the time of next calculation.

The MER is deducted from the total value of the portfolio before the Net Asset Value (or individual share price) is calculated. Although the MER is expressed as a percentage per year, it is calculated and charged daily. The daily expense deducted from the fund’s portfolio is calculated by the following formula:

Therefore, approximately $147,379 is taken from TDB161 each day to cover the management fee and operating expenses (Note: this expense value is an estimate because the portfolio value fluctuates on a daily basis due to market activity).

After the MER of $147,379 has been deducted, the remaining money invested is divided among all remaining shares to calculate day’s the Net Asset Value. The published rates of return for any given mutual fund are calculated only after the MER has been deducted. The MER is charged regardless of the fund’s performance, including if it decreases in value.

Investor’s Perspective

If I had $5000 invested in TDB161, my investment carries an estimated weight of 0.00020% of the entire portfolio value ($5000 / $2,467,591,691). My portion of the investment would be responsible for $0.30 of the $147,379 collected in fees for the day. For simplicity sake, my MER can be calculated as a percentage of my entire investment holding (2.18% x $5000), amounting to approximately $109 in fees for the year.

Impact of MER Over Time

To quantify the effect of a MER over a long period of time, let’s consider an investing scenario with the following assumptions:

- An annual $1,000 contribution made in a mutual fund for a period of 10 years;

- 5% annual rate of return (ROR) on the investment; and

- MER of 2.18%.

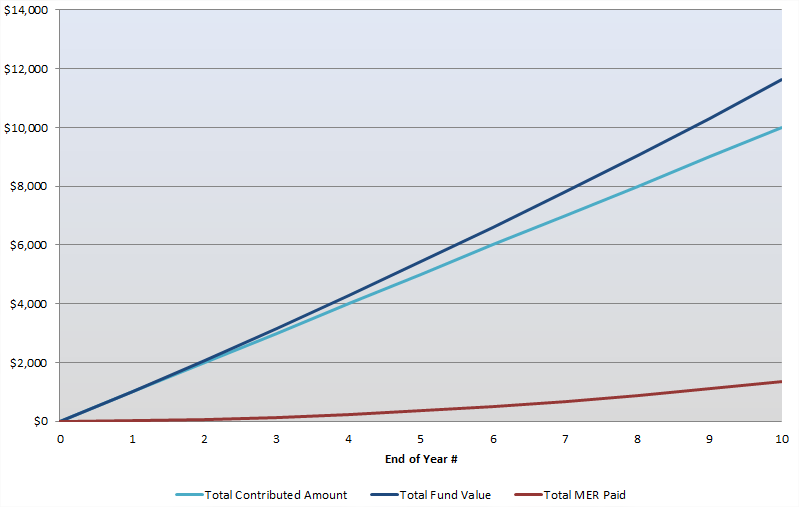

A summary of the fund’s performance after a duration of 10 years is shown in the table below:

[table th=0]

Total Contribution, “$10,000”

Total Fund Value*, “$11,619”

Total MER Fees Paid, “$1,367”

Percent of MER Fees on Total Contribution, 14%

Percent of MER Fees on Total Fund Value, 12%

*Note:, MER deducted [/table]

The money invested grows to $11,619 after the deduction of the MER. The total amount of MER fees paid is 12% of the total fund value ($11,619) and 14% of the total contribution amount ($10,000). The percentage of cumulative MER paid continues to increase as the investing duration increases. MER has the same compounding effect as RORs, but in the opposite direction, and subsequently, decreasing the returns and net ROR.

The following graph illustrates the growth of the investments as well as the cumulative MER each year.

Want to see how much fees you are paying? Get the INVESTMENT GROWTH CALCULATOR!

A Tale of Two Fees

To put things into perspective, let’s compare the effects of a high MER versus a low MER. Consider two different scenarios with the following assumptions:

- An annual $1,000 contribution made in each mutual fund for a period of 10 years;

- 5% annual ROR on the investments;

- Scenario A has a MER of 2.18%; and

- Scenario B has a MER of 0.33%.

A summary of the both fund’s performance after a duration of 10 years is shown in the table below:

[table]

Scenario, A, B

MER, 2.18%, 0.33%

Total Contribution, “$10,000”, “$10,000” Total

Fund Value*, “$11,619”, “$12,952”

Total MER Fees Paid, “$1,367”, “$220”

Percent of MER Fees on Total Contribution, 14%, 2.2%

Percent of MER Fees on Total Fund Value, 12%, 1.7%

*Note:, MER deducted, “” [/table]

The exact same amount invested each year. The exact same ROR. The exact same investing duration. In Scenario A, the investments grows to $11,619 where as in Scenario B, the investment grows to $12,952! Scenario B’s return is $1,333, which accounts to 11%, more than Scenario A. All because of the difference in MER.

Last Word

As much as it’s important for an investor to recognize the ability for assets to generate earnings, it is just as important to understand the negative effect of MER on investments. It handicaps the investment by eating into the ROR and leaving less assets to be compounded positively. A percentage point on a small annual contribution (like $1000) may seem insignificant, but a percentage point on of a lot of money is a lot of money, especially in the long-term. A 2.18% MER fund consumes 14% of the original contribution over 10 years; extend the investment period to over 25 years, the MER consumes 37% of the original contribution. The little things add up over time. The MER matters. In fact, it matters a lot. It matters even more when investing long-term. Do your investments a favour and choose a low management expense ratio fund when investing. If you want to see how the MER of your investments will impact your porfolio over time or compare the total fees paid for two different MERs, download our free Investment Growth Calculator.

I hadn’t heard of this term or valuation – thank you for that, Daniel! Just one more thing for us to remember as we learn to educate ourselves on investing. 🙂

I’m glad you found the information helpful, Laurie. It’s a tough egg to crack, but once we figure out the ins and outs, there’ll be no stopping us will there!

Yep, I know the MER matters! I just started looking into pension plan fees, and they’re not horrendous. They’re not 0.33%, but they’re under 1%, so I was happy to see that.

That’s great to hear that your plan is looking out for you in a good way. Keep up with the savings!

the 5% ROR is that net fee’s? If it is then I don’t understand how MER’s matter. If so then Fund A had a gross return of 7.18 before fees, and fund B had a gross return of 5.33…. either way in the end they were both returning 5%. I appreciate any answers I receive as this is confusing to me.

@Eric

You are correct; the 5% ROR is net fees. Should Fund A and B have respective gross returns of 7.18%/5.33% they would both result in 5% return after fees. Note that Fund A has to outperform Fund B by 1.85% to net the same return.

It also works in reverse. If Fund A and Fund B results in a net return of -5%, it would still cost 2.18%/0.33% for being invested in the fund, dragging your returns to -7.18%/-5.33%.

A lower MER means that more of money remains invested rather than going towards paying fees. A higher MER will result in higher cumulative costs over the long term.

Hope this helps.

Great explanation Daniel. Amazing how long the industry has been able to pull the wool over investors eyes! Also of note is that Canadians pay the highest MERs of any developed country. Do you know why? Me neither! Come on, CRM2.

Steve

Thanks Steve. I have no idea either. Many don’t take the time to understand fees they’re paying much less fees in other countries. Thankfully things will start to shift with CRM2. It’s going to be interesting watching the industry react!