When I was a kid, my dad’s idea of fun was to teach his children math and science (he still reads anatomy and medical textbooks as a hobby. Serious). He first introduced me to compound interest when I was about eight years old.

“If you saved $100 every year and the interest rate was 10%, how much money would you have in 5 years? 10 years? See how it has grown?!” My dad wanted me to see the magic of compound growth1.

I didn’t. I did the math exercises because I was promised popsicles. When the “fun” was done, I went on my merry way to play. When I was a bit older, I would always grimace at the mention of “compound interest,” recollecting memories of calculations- done by hand- while other kids watched TV (We never had cable at home; it was an expense my dad wasn’t willing to pay). Now, as an adult and a parent myself, I hope my dad will be willing to teach my kids math and the magic of compound growth. Because, boy, is it magical!

How the Magic of Compound Growth Works

Albert Einstein referred to compound interest as the “the most powerful force in the universe.” It is the concept of money that continually generates earnings. An initial sum of money earns interest. Over time, that interest also earns interest; it’s a snowball of growth earning growth!

Borrowing from Robert Brown’s Wealthing like Rabbits, imagine an island with no rabbits- not a single one. If you were to introduce a few onto the island and let the rabbits do what they do best, how many rabbits would you think would there be on the island after 60 years? That, in a nutshell, is the magic of compound growth.

“Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.”

– Albert Einstein

For example, suppose I saved $100 and it gains $5 in interest, at the end of the compounding period- say a year- I will have a total of $105. The $105 then gains interest over the next year. By the end of the that period, I will have earned another $5.25 and my total will have grown to $110.15.

Okay, that doesn’t seem like much so let’s look at larger sums of money over a longer period of time. Let’s say I invest $3,000 with an interest rate of 5% into Little Sister’s RESP on the day she was born. By the time she is ready for post-secondary school at 18 years later, the money will have grown to $7,219.86. That’s from doing absolutely nothing!

Let’s take it one step further. Say I continue to add to her RESP over time and invest $3,000 each year instead of just at the time she was born. At the end of 18 years, I will have invested a total of $54,000, but my investments will have grown to $88,617.01. If you get excited about finding $1 on the sidewalk, think of what you could do with an extra $33K. You’d have compounding interest to thank. In short, the more you save over a longer period of time, the more you will earn. This compounding is quite something, isn’t it?

Compounding Interest and Retirement

Do you want to see the real magic? Forget about the children (real or hypothetical) and see how much money you can have saved up for retirement. Let’s assume I start with no savings and there is another 35 years until I retire in my mid-sixties. If I invest $10,000 every year over 35 years, my nest egg will sit at $893,203 waiting for me to retire. MAGIC.

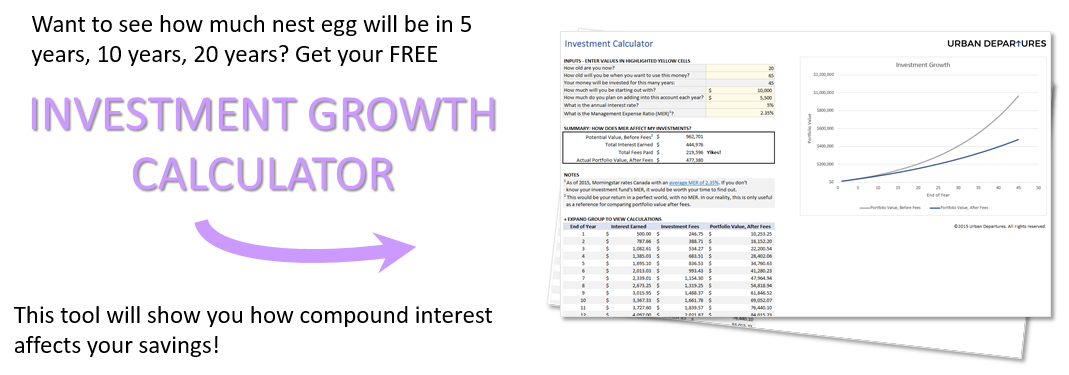

Interested in seeing how your money can grow? Play around with our nifty Investment Calculator to see how compound growth works. Even small amounts of savings can add up over time.

FREE INVESTMENT GROWTH CALCULATOR

The Last Word: Collect Interest, Not Dust

When Benjamin Franklin died in 1790, he bestowed $4,500 to the cities of Boston and Philadelphia. The money was held in trust and not to be touched for 100 years. After that, the cities could withdraw $500,000 from trust; the rest of the money had to remain untouched yet another 100 years. 200 years later, in 1990, each city’s endowment was worth over $2 million. Now, you won’t have 200 years to invest your money, but understanding the concept of compound growth will have a major impact on your financial success.

Check out our new Investment Growth Calculator and see how the magic can work for you!

Note:

1My dad also showed me how compound interest can work against me, like in the case of borrowing money or not paying off my credit cards (which is why I have always clear my balance at the end of the month). He also taught me how to build circuit boards, program in two different languages, and build websites, all before the average family had internet at home. Unfortunately for him, the only information I retained was some basic HTML, which was I guess was useful when I re-designed the website. Daddy, between never having consumer debt and saving money from not having to hire a designer for this website, be proud.